The past month I’ve been digging the carbon offset industry and came up with a map structured in three layers and a couple of subcategories:

- The buyer layer: entities that buy carbon offsets.

- The reseller layer: the companies and non-profit selling (but not producing) carbon offsets.

- The carbon project layer: the various entities that issue carbon offsets and also certify and finance carbon projects.

In the rest of the post, I describe and cover various trends happening in each layer of the stack. You can find the list of companies on this landscape (around 50) here.

1- The buyer layer

Description: in this layer, you find the different entities that buy carbon offsets to reduce their carbon footprint:

- Individuals: at the moment it’s probably a small share of people who are well informed about their carbon footprint and actively want to offset it.

- Businesses: large and small businesses that want to offset the carbon emissions generated by their activity whether it comes from their logistics, production lines or even their employee activity (corporate travels, offices, etc.).

Trend #1 consumers: an increasing number of people will buy carbon offsets.

The major trend happening in this layer is the increasing number of people and businesses that want to offset their carbon footprint. When it comes to the consumer side, it’s probably driven by a genuine will to contribute to fighting climate change. This is why I believe that more and more people will do it once buying carbon offsets becomes ubiquitous and better integrated into our everyday life: for example, when I buy a plane ticket or a pair of shoes I will have the choice to offset it directly in the checkout process.

Trend #2 businesses: the pressure to act for climate change will only grow for corporations.

When it comes to businesses, if you look at the past year only, plenty of large companies, from tech companies such as Amazon, Google or Microsoft to airline companies, have pledged to invest billions of dollars in carbon offsetting programs in the next decade. If these programs really materialize, there’ll be a huge influx of money in this industry. I also think that this trend will accelerate as businesses are forced to act under the pressure of their customers/stockholders/society (and surely regulation in the near future).

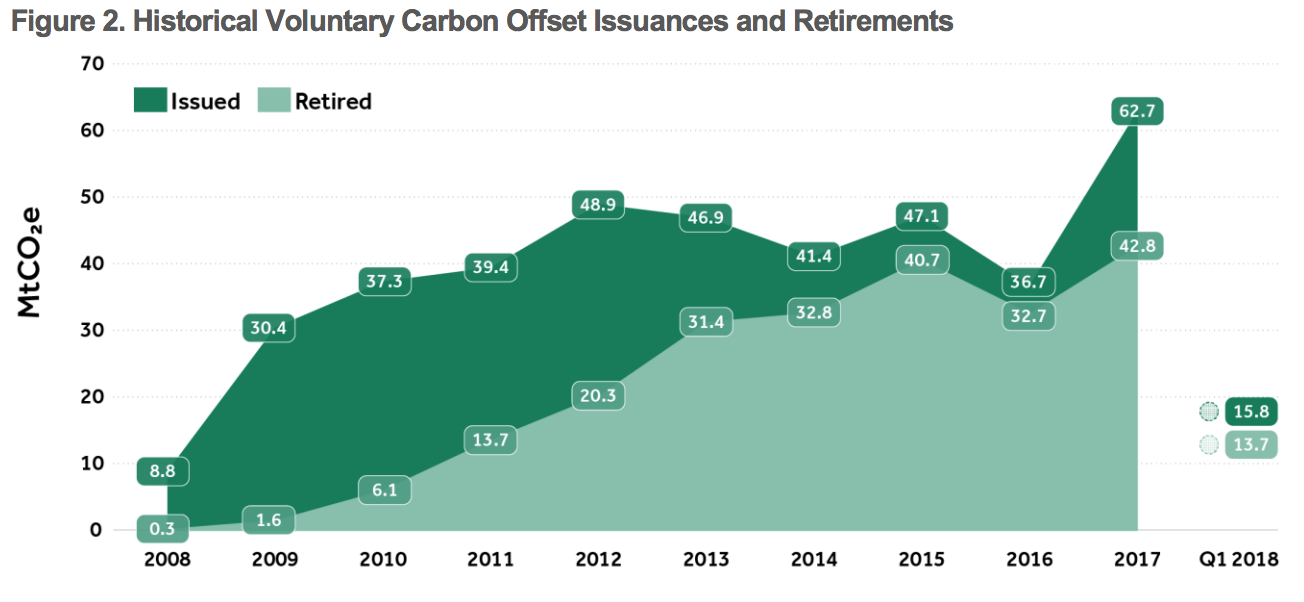

The number of carbon offsets produced and bought kept growing the past 10 years:

2- The reseller layer

2.1 Horizontal resellers

Description: Now if a person or a business wants to offset its carbon footprint, how does he do? Chances are that he’ll do a Google search (like I did :-)) and find a myriad of websites that offers a carbon footprint calculator (basically a form that you fill to estimate how much carbon emissions your lifestyle or business activity generates), and based on the result, will tell you to pay a certain amount of money that will be reinvested in carbon offset programs such as afforestation (planting trees), landfill gas capture, renewable energy or new farming practices. The amount you pay is supposed to cover the carbon your lifestyle emits (the more you produce, the more you pay).

The vast majority of these websites are carbon offset resellers. They are not the companies that will plant trees thanks to your money. They actually buy carbon offset credits directly with the carbon project developers/operators (the companies which plant trees or run wind farms) and resell them to you. For example, let’s say that it costs 100$ for a certified tree planting program to plant enough trees to capture one ton of CO2. If the reseller wants to buy the equivalent of 200 tons of carbon offset, they will pay $20k to the afforestation program and this is what they resell to you.

When it comes to this reseller layer, there are two main models:

- Direct resellers: they resell carbon offsets directly to consumers.

- Marketplaces: they connect buyers and carbon project developers.

Trend #1: A new generation of carbon offset resellers

The first obvious trend happening is the emergence of a new generation of carbon offset resellers. This model exists for a while now, but the majority of them offer a poor customer experience (very rough, lots of product friction) and lack transparency as you have to read the fine print to understand how your money is used. A new generation of products in that category (Wren, Compensate, Pachama) is emerging. These startups don’t disrupt the reseller model itself but focus on providing a better user experience (from better product to more transparency and community aspects). To be honest, this space will probably be the most crowded, and the main differentiation brought by most startups (better buying experience) makes me think that they are really “marketing” companies that need to be the best at attracting eyeballs and converting them. The big question is whether, as consumers, we need so many of them if they don’t really differentiate.

Trend #2: Automating the input process

When it comes to estimating carbon footprint, one of the major problems is that it’s a tedious process for the user. Most of the time you need to enter plenty of data points manually in long forms. In my opinion, this is a major product friction for broad adoption. Several companies try to address this problem by automating the input process. For example, Reduce is a mobile app that connects to your bank account and analyzes your purchase history to estimate your carbon footprint automatically. offCents automates this process for transportation by leveraging the geolocalisation data coming from your mobile phone. I believe that it’s the direction we’re heading: aggregating more and more data sources to automatically estimate an individual or a business footprint.

2.2 Specialized resellers

Description: We’re also seeing an increasing number of startups focused on addressing carbon footprint for specific use cases or industries. It turns out that estimating precisely the carbon footprint of a person or a business is a complex task that depends on many different parameters, data references and the methodology used (ex: GHG protocol, Defra, Berkeley Cool Climate…). This is why we’re seeing a number of resellers trying to innovate on that front.

Trend #1: More specialized calculators & resellers

Since estimating carbon footprint depends on many parameters, it makes sense to have calculators dedicated to specific use cases such as traveling (see TriptoCarbon or Atmosfair), diet habits, energy consumption or even to estimate the carbon footprint of a website. Going very deep into carbon footprint calculation might not make sense for an individual, but imagine for a business that wants to offset the corporate travels of its hundreds of employees. When you’re likely to pay hundreds of thousands or even millions of dollars for your carbon offsetting program, you need a more reliable and accurate estimation. These “verticalized/specialized” resellers make sense from that perspective.

Trend #2: “Carbon offset program as a service” for businesses

The majority of the startups I shared just above target consumers. However, businesses have different needs and estimating the carbon footprint of a company is more complex than for an individual. While big companies such as Amazon, Google or Microsoft have the resources to plan and execute on their carbon offset program internally, it’s not the case for most small and medium-sized businesses. This is why in this layer we also have a number of resellers specialized in carbon offset programs for businesses. They offer tailored carbon footprint estimation and help businesses set up and execute their carbon offset programs. I expect more “business carbon offset program as a service” companies to emerge (from setting it up to reporting).

3- The carbon project layer

3.1 Carbon project developers & operators

Description: carbon project developers & operators are the entities (companies or nonprofits) that develop and operate the wind farms, landfill gas capture, and other afforestation programs. We can distinguish large carbon project players, such as South Pole, which oversee tens or even hundreds of carbon projects, from the small operators which run a single carbon project. At the moment the main types of carbon projects developed are around forest conservation and restoration, renewable energy, community energy and water, and waste transformation.

Trend 1: Large project developers going full-stack.

If you go on the website of the larger project developers such as South Pole or TerraPass you’ll notice that they offer a range of services that go beyond carbon project development. They also offer consulting services for businesses or even direct carbon offset purchases. If the carbon offset market continues to grow, I wouldn’t be surprised to see some large developers adopting a full-stack approach and integrate more components of the value chain. This “full-stack” approach can also happen at the reseller level (reseller integrating carbon project development).

Trend 2: small carbon project operators need more “as a service infrastructure”

If the carbon offset market grows, we’ll probably see an increasing number of small carbon project operators being created. These operators don’t have the same resources as the large developers, so we could potentially see an ecosystem of infrastructure services and tools (from marketplaces to financing and certification services) emerge to support this small carbon project operator segment.

3.2 Certification & Verification

Description: carbon project developers need to follow rules and guidelines in order to have their project certified. In the certification component you have two types of entities:

- Standard and certification bodies: the entities (most of the time nonprofit organizations) that set the guidelines to ensure projects make measurable contributions to offsetting carbon emissions.

- Accredited third-party certification bodies: the agencies and other entities that assess and certify carbon projects as well as make sure that they continue to be “compliant” (the continuous reporting aspect).

Trend 1 – Certification: Simplifying the certification process

For a carbon project, the certification process is quite complex (just try to navigate the myriad of PDFs on the Gold Standard dedicated page) and costly. For bigger/well-funded carbon projects it might not be a huge issue, but for the majority of small to medium size projects, this is a real problem. Another issue related to the verification process is that many initiatives cannot be certified because they do not meet the requirements set by the major certification bodies, despite the fact that they do have a positive effect on carbon emissions. I haven’t dug this aspect much, but we’ll probably see many changes happening on that side (easier ways to certify a project and more carbon initiatives categories taken into account).

Trend 2 – Verification: Better ways to monitor carbon project efficiency

One of the major issues raised by carbon offset detractors is that once a carbon project is certified, it’s sometimes hard to follow/monitor if it continues to deliver on its promises. How do you make sure that the trees planted are growing well and taking care of in the long term? How do you make sure that the solar panels you built in rural communities are still working two years later? These are not easy challenges to address, but we’re also seeing innovation on that side. For example, Pachama “develops machine learning algorithms that analyze satellite images of forests to provide accurate estimations of carbon storage and capture to provide additional verification.” Satellite imagery, but also IoT will probably play a big role in tackling the monitoring challenge. Measuring the results and monitoring the efficiency of carbon projects are key aspects as carbon offsetting is often criticized as “greenwashing”. You need to establish more trust based on real metrics.

3.3- Financing

Description: I haven’t dug this component enough, so I won’t write about it too much. But for sure we need more capital invested in carbon projects. If you take renewable energy projects alone: “Global investments into renewables worldwide topped $282 billion, up 1% from 2018. Developing the energy system required to meet rising demands and prevent 2 ˚C of warming will require annual clean energy additions to quintuple by 2040” Source.

Conclusion: what do I think about this space?

While I found it super interesting to try to understand the carbon offset stack (I am by no means an expert, I just think I understand it a bit better), I had two growing concerns while exploring this space.

Greenwashing. Carbon offsetting is far from being perceived as the panacea when it comes to fighting climate change. The major problem behind this model is that offsetting your carbon footprint does not reduce your carbon emissions. You basically pay to cover what you produce, and in that perspective, it doesn’t prevent companies or individuals from actually increasing their carbon emissions. They’ll just pay more to cover their increase and say that they are carbon neutral. This is a huge issue for the whole industry IMO. Just to be sure, I’m not criticizing the carbon projects themselves, which I think are crucial to fight climate change, but the offsetting model itself. One could argue that regulation could help in that regard, for example by limiting the share of carbon offset a company can leverage compared to the real “decarbonization” investments they need to do.

In any case, this is why I am becoming more and more interested in startups that actually help businesses lower their carbon emissions and not just offset it. There’s a growing number of startups that enable businesses (especially in “carbon emission heavy” industries such as textile, cement, construction, transportation…) to improve their environmental impact while also saving costs (for example by lowering production scraps or by improving processes efficiency). Their business model seems more straightforward too. (And yes, I’m aware that even this approach can have its drawbacks in the form of the rebound effect).

Business model. TBH I didn’t study the economics of the different players in the various layers, but I find it hard to justify that a company in the carbon offset stack generates high margins. When you’re a consumer (an individual or a business), you want that a maximum of your money actually goes to fighting climate change and not for middlemen to make a big profit. While it’s not a problem if the company is a non-profit organization (like many are in my landscape), it can be a major problem if it’s a VC backed startup. This aspect would require a whole deep dive by itself. A potential solution to my concern is if the carbon offset aspect is given for “free” (the startup generates no margin on it), and the product monetizes other aspects. For example, Doconomy is a credit card with carbon offset features, so they can monetize different aspects other than the carbon offsetting feature.

As a conclusion, despite my concerns, I believe that this industry will grow in the next few years, driven by the massive investments announced by many large companies (also consumers) and probably also by increasingly restrictive regulations pushed by governments around the world. Buying carbon offsets will be the easiest way for the majority of companies to comply with coming carbon reduction regulations. That being said, from a VC perspective, I don’t find this space obvious at all. Many investors are looking to invest in carbon offset startups, but I’m not sure that many of them are compatible with the VC model. I discussed this issue with some VCs and several told me that what they really bet on, is that massive companies could be built in that space thanks to network effect (between consumers/businesses and carbon projects) or technological breakthrough (better carbon capture tech for example). The economics of many of these companies might not be clear now, but the climate problem is so huge that if they manage to scale they’ll figure it out after.

Companies on the landscape

Reseller Layer

- Horizontal

- Specialized

Carbon Project Layer

- Developers and operators

- Certification/standards